Why Most Travelers Assume They’re Covered (But Aren’t)

There’s a moment every traveler experiences right before a trip—the quiet confidence that everything is handled. Flights are booked, hotels are confirmed, and payments are done with a credit card that promises “travel benefits.”

It feels like protection is built in.

But here’s where reality often catches people off guard.

Many travelers believe that using a credit card like the Bank of America Travel Rewards card automatically means full travel insurance. In truth, what they have is something much lighter—basic protections that only cover a small part of what can actually go wrong.

And the difference between “basic protection” and “real coverage” only becomes clear when something unexpected happens.

What Bank of America Travel Rewards Travel Insurance Actually Is

A rewards card first, protection second

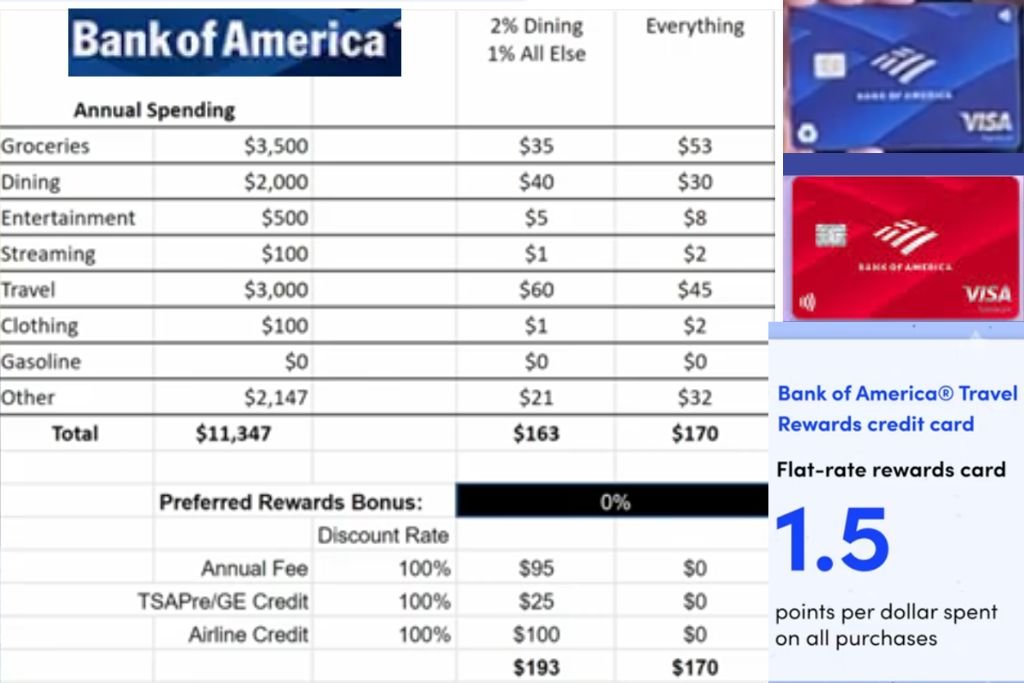

To really understand this card, you have to start with its purpose. The Bank of America Travel Rewards Credit Card was designed to be simple and accessible. It gives you flat-rate rewards, no annual fee, and easy redemption options.

Insurance was never its main focus.

What you get instead is a set of limited travel protections, mostly tied to Visa benefits. These are helpful in certain situations, but they are not designed to fully protect you from financial loss during travel.

Think of it like this:

It’s not a shield—it’s more like a thin layer of padding.

The Coverage Gap: What You Have vs What You Actually Need

Why this gap matters more than people think

One of the biggest mistakes travelers make is assuming “some coverage” is enough. But when you compare what the card offers with what’s actually recommended, the gap becomes very clear.

| Insurance Type | Card Coverage | Recommended Coverage |

|---|---|---|

| Trip Cancellation | $0 | $5,000 |

| Emergency Medical | $0 | $100,000 |

| Trip Interruption | $0 | $5,000 |

| Trip Delay | $0 | $1,000 |

| Baggage Delay | $0 | $1,000 |

| Baggage Loss | $0 | $1,000 |

| Travel Accident | Limited | $1,000,000 |

This isn’t just a small difference—it’s a complete absence of protection in the areas that matter most.

And that’s what makes this topic so important.

Before Your Trip: What Happens If Life Gets in the Way

Trip Cancellation Insurance

Why this is one of the most important protections

Life doesn’t always go according to plan. You might get sick, a family emergency might come up, or something unexpected might make it impossible to travel.

That’s where trip cancellation insurance becomes critical.

It allows you to recover:

- Flight costs

- Hotel bookings

- Prepaid reservations

With the Bank of America Travel Rewards card, this protection simply doesn’t exist.

What that means in real life

Imagine planning a $3,000 vacation and having to cancel just days before departure. Without insurance, every non-refundable expense becomes your loss.

It’s not just inconvenient—it’s financially painful.

During Your Trip: When Things Start to Go Wrong

Travel rarely goes perfectly. Flights get delayed, luggage gets lost, and plans change. This is where strong travel insurance proves its value—but this is also where this card shows its limitations.

Baggage Delay Insurance

Why delayed luggage is more than just an inconvenience

When your luggage doesn’t arrive, you don’t just wait—you need to act. Clothes, toiletries, chargers—these become immediate necessities.

With proper insurance, these emergency purchases are reimbursed.

With this card, they are not.

The real impact

What seems like a small issue can quickly turn into unexpected expenses, especially if delays last longer than a day.

Baggage Loss Insurance

Losing your luggage means losing more than belongings

A lost suitcase often contains items of both financial and personal value. Replacing everything can be expensive and stressful.

Without coverage, there’s no safety net.

You rely entirely on airline compensation, which is often limited and slow.

Trip Delay Insurance

Delays don’t just waste time—they cost money

Flight delays can force you to:

- Book hotels

- Pay for meals

- Arrange transportation

Good travel insurance absorbs these costs.

This card typically does not.

Why this matters

Even a single delay can turn into a chain of expenses that you didn’t plan for.

Travel Accident Insurance

The most misunderstood benefit

This is one of the few protections included, but it’s often misunderstood.

It covers extreme cases like serious injury or death during travel. However, it does not help with everyday medical needs.

What people expect vs reality

Most travelers assume this means “medical coverage.”

In reality, it’s a very specific and limited form of protection.

On Your Trip: When Situations Become Serious

This is where the stakes are highest—and where the lack of coverage becomes most noticeable.

Emergency Medical Insurance

Why this is the biggest missing piece

Medical emergencies abroad are not rare—and they are often expensive.

Without insurance:

- You may need to pay upfront

- Costs can escalate quickly

- Access to care may be limited

This card provides no support here.

Trip Interruption Insurance

When your trip is cut short unexpectedly

Emergencies don’t just stop trips—they complicate them.

You may need to:

- Book last-minute flights

- Lose hotel bookings

- Rearrange your plans

Without interruption coverage, all these costs fall on you.

Medical Evacuation and Repatriation

The scenarios people don’t like to think about

In serious cases, you may need to be transported to a better medical facility or even back to your home country.

These services can cost tens of thousands of dollars.

And this card does not cover them.

Rental Car Insurance: Where the Card Actually Helps

Collision Damage Waiver (CDW)

A practical and useful benefit

This is one area where the card provides real value.

If your rental car is damaged or stolen, the card can cover repair or replacement costs.

But there are limits

It does not cover:

- Injuries

- Liability

- Damage to other vehicles

So while helpful, it is not complete protection.

The Bigger Picture: What This Card Is Really Designed For

Understanding its true role

Once you step back and look at everything, a clear pattern emerges.

This card is designed to:

- Earn rewards

- Keep costs low

- Offer basic convenience

It is not designed to:

- Protect you fully

- Replace travel insurance

- Handle major financial risks

And that’s okay—as long as you understand it.

Should You Rely on This Card Alone?

The honest answer

For most travelers, relying solely on this card is not enough.

Especially if:

- You’re traveling internationally

- Your trip is expensive

- You want peace of mind

Adding travel insurance is not just a recommendation—it’s a practical decision.

Final Thoughts: The Difference Between Feeling Safe and Being Protected

There’s a subtle but important difference between feeling protected and actually being protected.

The Bank of America Travel Rewards Credit Card gives you just enough benefits to feel secure—but not enough to truly protect you when things go wrong.

And that’s where awareness becomes your best tool.

Before your next trip, take a moment to look beyond the surface. Understand what you have, what you don’t, and what risks you’re willing to take.

Because travel is unpredictable—but your preparation doesn’t have to be.

At Infoaxis, we focus on breaking down financial tools in a way that helps you make smarter, more confident decisions—especially when it matters most.

Read More : Connectivity Issues HSSGamepad

Read More : UploadArticle.com Authors

Leave a Reply